Michael Saylor recently defended Strategy’s credit model that is backed by Bitcoin, amid criticism suggesting that the company’s dividend structure, which utilizes STRC, resembles a Ponzi scheme. He clarified that the foundation of the business is centered on leveraging Bitcoin capital gains rather than relying solely on continual equity issuance.

In an interview shared on social media on May 9, Saylor responded to the market’s reaction following Strategy’s latest earnings call. During this call, the company indicated its preparedness to sell Bitcoin if necessary to fund dividends for its STRC preferred instrument. This proposal received significant attention due to Saylor’s well-known stance of “never sell your Bitcoin.”

According to Saylor, the more accurate expression of his view is that Strategy does not plan to be a “net seller” of Bitcoin.

“I often say, never sell your Bitcoin. The internet went wild when we mentioned selling it,” Saylor explained. “But if I were to be more precise, I should say never be a net seller of Bitcoin. It just would not have resonated as much.”

Addressing Criticism: Why Strategy is Not a Ponzi Scheme

The debate intensified after critics like Peter Schiff suggested that Strategy’s potential sale of Bitcoin to support STRC dividends undermined the sustainability of its business model. Saylor countered this perspective, asserting that the financial structure should not be interpreted as having Bitcoin assets effectively rendered worthless.

“If you possess $65 billion in assets, it’s quite unjustifiable for others to value it at zero,” he pointed out. “We want credit rating agencies to recognize that we possess substantial assets, not nothing.”

He outlined the crux of their business model: Strategy issues credit, uses the proceeds to invest in Bitcoin, and anticipates that Bitcoin’s value will appreciate over time, outpacing the costs associated with dividends. This approach can be likened to a real estate development firm that raises capital via credit to acquire land, improve it, and later profit from its appreciated value.

“Our aim is to clarify that we sell credit to make a capital investment in Bitcoin, which is a form of digital capital,” Saylor emphasized. “The value of this investment is expected to grow faster than the dividends, enabling us to monetize those capital gains for dividend payment.”

This differentiation is vital to Saylor’s rebuttal against Ponzi allegations. He believes critics often confuse the practice of using common equity to fund dividends with the underlying economic structure of the business. Historically, Strategy utilized MSTR equity, which he described as a derivative of Bitcoin, to fund dividends. However, he stressed the company’s intention for markets to understand it can also utilize Bitcoin directly.

Even if Strategy were to sell Bitcoin for dividends, Saylor maintains that the issuance of credit will facilitate the purchase of significantly more Bitcoin than it sells.

“If we sell a portion of our holdings to issue Stretch credit equating to 2.3% of our Bitcoin assets, we will still be net purchasers of Bitcoin in perpetuity, even while paying dividends,” he stated. “If Bitcoin appreciates by 2.3% annually, we can indefinitely cover the dividends without liquidating any common equity.”

Saylor mentioned that Strategy raised $3.2 billion from STRC in April, while the monthly dividend obligations were around $80 million to $90 million. This scenario means the company would essentially be “buying 30 Bitcoin while selling only one,” resulting in a net increase in holdings.

The interview also addressed Schiff’s critiques directly. Saylor asserted that Schiff’s fundamental issue arises from a skepticism towards btc itself, which makes it unlikely for him to accept any credit instrument predicated on it.

“Peter perceives Bitcoin as a Ponzi scheme and is not genuinely invested in the cryptocurrency space,” Saylor remarked. “Bitcoin represents digital capital, and we have established a digital treasury company by selling equity and credit mechanisms to acquire this capital. I believe Bitcoin will endure as it symbolizes wealth in a tokenized format with complete property rights.”

In conclusion, Saylor described STRC as a unique form of “digital credit,” meticulously designed to mitigate some of the inherent volatility of Bitcoin while securing a predictable yield. He noted that Strategy adopts an overcollateralization strategy, selling “$1 of credit” for every “$5 of Bitcoin” held.

“If one dismisses Bitcoin as a legitimate asset, they will invariably question the credibility of any financial vehicle associated with it,” he concluded. “However, for those who recognize Bitcoin as digital capital that serves as a store of economic wealth in tokenized form, our operations are quite straightforward.”

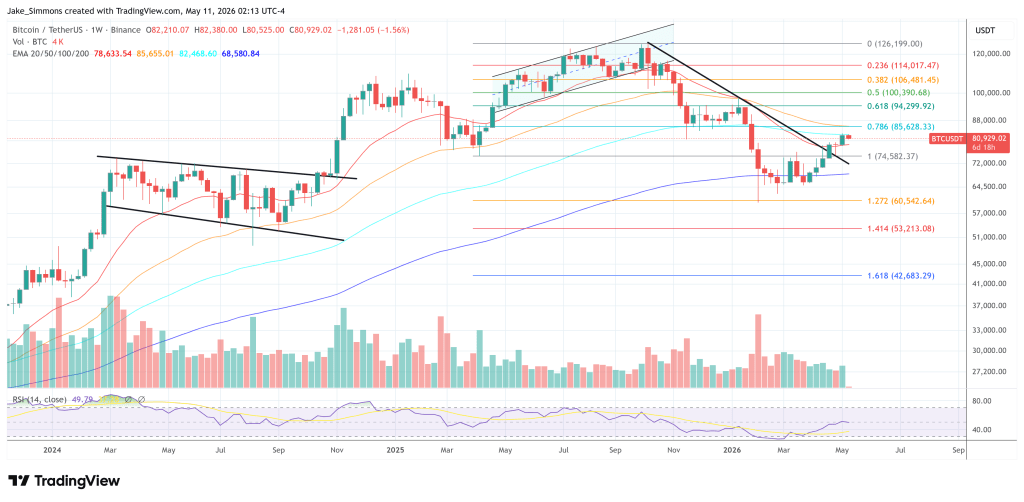

As a final note, Bitcoin traded at $80,929 at the time of this writing.